Post-Incorporation Compliances under the Companies Act, 2013

Establishing a company is a significant milestone for entrepreneurs and business enthusiasts. However, it’s just the beginning of a long journey. Once your company is incorporated, you are required to adhere to various legal formalities and obligations. These post-incorporation compliances are governed by the Companies Act, 2013, which is the cornerstone of corporate regulations in India. In this comprehensive guide, we will explore the intricate world of post-incorporation compliances under the Companies Act, 2013, and how they play a pivotal role in the life of a company.

1. Understanding the Companies Act, 2013

Before delving into the specifics of post-incorporation compliances, let’s establish a fundamental understanding of the Companies Act, 2013. It replaced the archaic Companies Act, 1956, and introduced a modern regulatory framework for businesses in India. The Act comprises several chapters and schedules that cover various aspects of company formation, governance, and dissolution.

2. Some key highlights of the Companies Act, 2013 include:

a) Classification of Companies: The Act categorizes companies into different types, such as public companies, private companies, and one-person companies, each having distinct compliance requirements.

b) Corporate Governance: It sets guidelines for corporate governance, including the appointment of directors, responsibilities of the board, and disclosure requirements.

c) Share Capital and Dividends: The Act outlines rules related to share capital, dividends, and fundraising through issues of securities.

d) Audit and Financial Reporting: It mandates regular financial audits and establishes accounting standards for accurate financial reporting.

e) Corporate Social Responsibility (CSR): The Act requires certain companies to allocate funds for CSR activities.

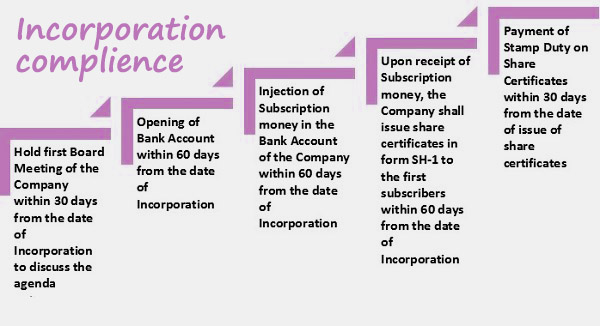

3) Post-Incorporation Compliances: A Necessity, Not a Choice

Once your company is incorporated, you must adhere to various post-incorporation compliances. These obligations are critical for maintaining the legal and financial health of your business. Failing to meet them can result in penalties, legal troubles, and even the dissolution of your company.

3.1. Obtaining the Certificate of Commencement of Business

Before a company can commence its business operations, it must obtain a Certificate of Commencement of Business. This requirement is primarily applicable to public companies and private companies that issue shares to the public. To obtain this certificate, you must fulfill the following conditions:

- File a declaration with the Registrar of Companies (RoC) stating that the subscribers to the memorandum have paid the value of shares agreed upon.

- Submit a verification of registered office address to the RoC.

3.2. Appointment of Statutory Auditors

Every company, irrespective of its size, must appoint a statutory auditor within 30 days of incorporation. The auditor is responsible for examining the company’s financial statements and ensuring compliance with accounting standards.

3.3. Holding Board Meetings and General Meetings

Regular board meetings and general meetings are essential for decision-making and shareholder communication. Companies must conduct at least one board meeting in every three calendar months and an annual general meeting (AGM) within six months of the end of the financial year.

3.4. Statutory Registers and Records

Companies are required to maintain various statutory registers and records, including the Register of Members, Register of Directors and Key Managerial Personnel, and Register of Charges. These records must be kept up to date and made available for inspection by authorities when necessary.

3.5. Filing of Financial Statements and Annual Returns

One of the most critical post-incorporation compliances is the timely filing of financial statements and annual returns with the RoC. These documents provide a snapshot of the company’s financial health and must be filed within prescribed timelines.

4) Compliances Based on Company Type

The compliance requirements under the Companies Act, 2013, vary depending on the type of company. Let’s take a closer look at these differences:

4.1. Public Companies

Public companies have more extensive compliance obligations compared to private companies. Some key compliance requirements for public companies include:

- Appointment of independent directors.

- Formation of various committees, such as the audit committee and nomination and remuneration committee.

- Compliance with the minimum public shareholding requirements.

4.2. Private Companies

Private companies have certain relaxations when it comes to compliance. However, they must still adhere to several essential requirements:

- Minimum two directors.

- Maintenance of the Register of Members.

- Restriction on the transferability of shares.

- Limitation on the number of members (maximum 200).

4.3. One-Person Companies (OPCs)

OPCs are a unique concept introduced by the Companies Act, 2013. They are designed to facilitate single-person entrepreneurship. Key compliances for OPCs include:

- Nomination of a nominee director.

- Annual filing of financial statements and annual returns.

- Restrictions on converting an OPC into any other type of company.

5. Compliance Timelines

Compliance timelines are sacrosanct under the Companies Act, 2013. Failure to meet these deadlines can result in penalties and legal consequences. Some important compliance timelines include:

5.1. Annual General Meeting (AGM)

All companies must conduct their AGM within six months from the end of the financial year. During the AGM, financial statements and annual returns are presented to shareholders for approval.

5.2. Financial Statements

Companies must prepare financial statements within 30 days of the AGM and file them with the RoC within 30 days from the date of the AGM.

5.3. Annual Returns

Annual returns must be filed with the RoC within 60 days of the AGM. These returns provide information about the company’s share capital, indebtedness, and changes in directorships.

5.4. Statutory Registers

Statutory registers, such as the Register of Members and Register of Directors, must be maintained and updated regularly throughout the year.

6. Penalties for Non-Compliance

Non-compliance with post-incorporation requirements can have severe consequences. The Companies Act, 2013, prescribes various penalties and legal actions for non-compliant companies, including:

6.1. Monetary Penalties

Companies may be subjected to monetary fines for late filing of documents, failure to hold AGMs, or non-maintenance of statutory registers.

6.2. Legal Proceedings

Non-compliance can lead to legal proceedings initiated by regulatory authorities or shareholders. These can result in fines, restrictions on the company’s operations, or even winding up.

6.3. Disqualification of Directors

Directors who are associated with non-compliant companies may face disqualification, preventing them from holding directorship in any other company.

Related Articles

7. Easing Compliance Burden

The complexity of post-incorporation compliances can be overwhelming, especially for startups and small businesses. However, there are several ways to ease the compliance burden:

7.1. Professional Assistance

Hiring a company secretary or a legal professional can help ensure that all compliance requirements are met on time.

7.2. Compliance Management Software

Many software tools are available to help companies track and manage their compliance obligations, sending reminders for filing deadlines and updating statutory registers.

7.3. Regular Audits

Conduct regular internal audits to identify and rectify compliance gaps before they become major issues.

Conclusion

Post-incorporation compliances under the Companies Act, 2013, are the cornerstone of good corporate governance in India. They ensure transparency, accountability, and legal compliance in the functioning of companies. While they may appear complex and demanding, adherence to these compliances is not optional but mandatory.

For entrepreneurs and business owners, staying compliant is not only a legal requirement but also a means to build a trustworthy and sustainable business. Neglecting these responsibilities can lead to severe consequences, including financial penalties and even the dissolution of the company.

Therefore, it is crucial for companies to invest time and resources in understanding, implementing, and staying updated with post-incorporation compliances. By doing so, they can build a strong foundation for growth and success while navigating the complex regulatory landscape of the corporate world.

In conclusion, post-incorporation compliances are not just legal formalities; they are the threads that bind the fabric of responsible corporate citizenship. Embracing them is not a choice but a necessity on the path to achieving corporate excellence and ensuring a prosperous future for your company.